Welcome to the Hahn Loeser CTA Hub, a central location to quickly find current and relevant information regarding the Corporate Transparency Act. The Corporate Transparency Act impacts most privately owned businesses, and may impact real estate deals, construction engagements, estate planning for business owners, labor and employment agreements and litigation.

The Corporate Transparency Act is federal legislation taking effect on January 1, 2024 that will impact most privately owned businesses. It requires certain beneficial ownership information pertaining to such privately owned companies be reported to the U.S. Treasury’s Financial Crimes Enforcement Network (FinCEN).

Most privately owned businesses will be subject to the CTA. Owners of privately owned businesses should consult with their attorney promptly to discuss the CTA and its impact on their business.

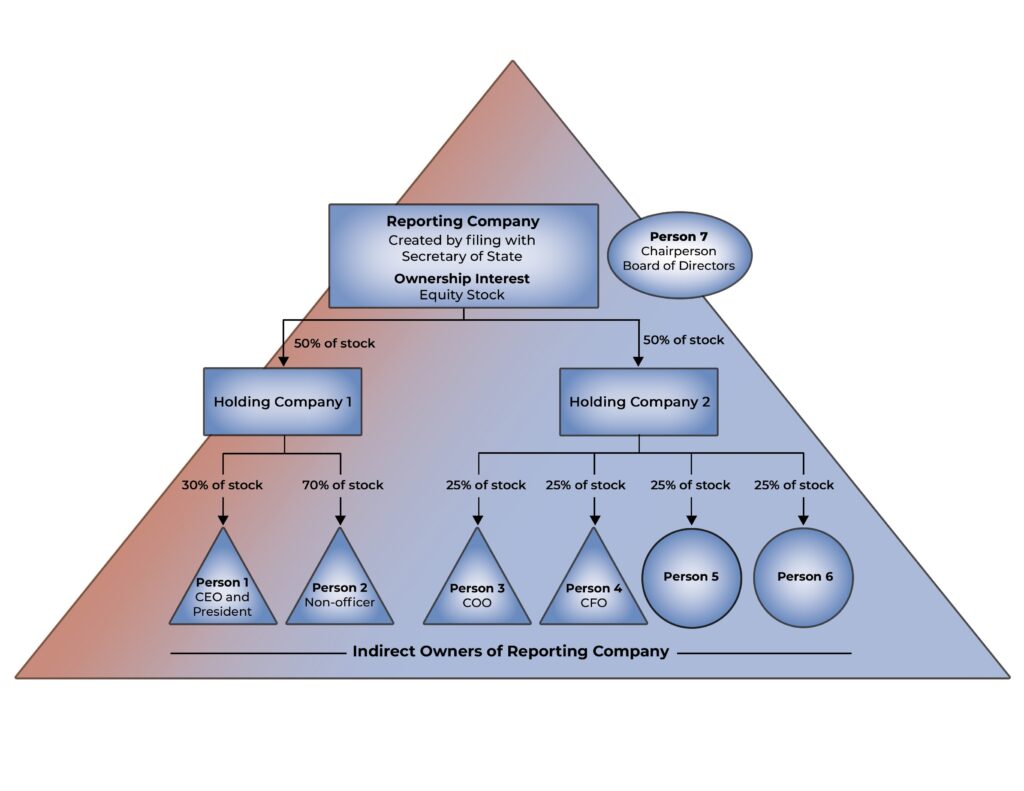

The Corporate Transparency Act (the “CTA”) is new federal legislation codified as 31 U.S.C. §5336, that requires most privately owned companies to disclose Beneficial Ownership Information (“BOI”) to the Financial Crimes Enforcement Network (“FinCEN”) of the United States Treasury.

All domestic or foreign entities that register with a state Secretary of State office in the United States (or similar office under the law of a State or Indian Tribe) may be subject to the CTA reporting obligations. The CTA applies to corporations, limited liability companies, partnerships, limited partnerships, certain trusts, and disregarded entities. A company subject to the CTA is known as a “Reporting Company.” (31 U.S.C. §5336(a)(11)(A))

There are twenty-three (23) enumerated exemptions whereby such entities are not subject to the CTA and therefore are not a Reporting Company. (31 U.S.C. §5336(a)(11)(B))

|

1. Securities Issuer |

13. State-Licensed Insurance Producer |

|

2. Government Authorities |

14. Commodity Exchange Act Registered Entity |

|

3. Banks |

15. Accounting Firm |

|

4. Credit Union |

16. Public Utilities |

|

5. Depository Institution Holding Company |

17. Financial Market Utility |

|

6. Money Services Business |

18. Pooled Investment Vehicle |

|

7. Broker or Dealer in Securities |

19. Tax-Exempt Entities |

|

8. Securities Exchange or Clearing Agency |

20. Entity Assisting Tax-Exempt Entity |

| 9. Other Exchange Act Registered Entity | 21. Large Operating Company |

| 10. Investment Company or Investment Advisor | 22. Certain Exempt Entity Subsidiaries |

| 11. Venture Capital Fund Adviser | 23. Inactive Companies |

|

12. Insurance Company |

Reporting Companies must disclose their business name, any assumed names (e.g., trade names or “dbas”), state of formation, and principal business address and its federal employer identification number.

Each Beneficial Owner of the Reporting Company has to report the following BOI to FinCEN:

A beneficial owner is any individual who, directly or indirectly, exercises “Substantial Control” over a Reporting Company or owns at least twenty-five percent (25%) of the Reporting Company’s ownership interests. (31 U.S.C. §5336(a)(3)(A))

As explained in FinCEN’s FAQ D.2., a person who exercises Substantial Control generally means any of the following:

The treatment of subsidiaries will depend on the facts and circumstances of how the subsidiary is owned by its parent company and what exemptions may apply to the parent. For example, if a subsidiary is wholly owned by an exempt company, the subsidiary will likely not have to report its BOI, but rather will only have to report that it is owned by an exempt entity. The subsidiary will have to report the name of the exempt parent company. (31 U.S.C. §5336(a)(11)(B)(xxii) and §5336(b)(2)(B). See also FinCEN FAQ #22)

An entity will qualify for the large company exception if ALL six (6) of the following criteria are satisfied:

An entity will qualify of the inactive company exception if ALL six (6) of the following criteria are satisfied:

Existing Reporting Companies have one (1) year to comply. That is, any entity formed before January 1, 2024, must file their initial report on or before December 31, 2024.

New Reporting Companies have ninety days (90) days to comply. That is, any entity formed on or after January 1, 2024, but before January 1, 2025, must file their initial report within ninety (90) days of formation.

Reporting Companies formed in 2025 and thereafter will have just thirty (30) days to comply. That is, any entity formed after December 31, 2024, must file its initial report within thirty (30) days of formation.

CTA compliance obligations are ongoing. Any change to any to a Beneficial Owner’s information must be reported to FinCEN within thirty (30) days of the change.

(see generally, (31 U.S.C. §5336(b)(1)

FinCEN may impose both civil and criminal penalties for failure to comply. Civil penalties may be up to five hundred dollars ($500) per day. Criminal Penalties include fines of up to ten thousand dollars ($10,000) and up to two (2) years in prison. CTA reporting obligations must be taken seriously. (see generally, 31 U.S.C. §5336(h)(3))